After back-to-back years of 20%-plus gains in 2023 and 2024, the S&P 500 clearly has bullish momentum heading into 2025. However, the S&P 500’s forward earnings multiple of 21.4 is also above its five-year average of 19.7, raising concerns about potentially bloated stock prices. In other words, stock selection may be critical for investors in 2025.

The 10 best stocks to buy included below are all recommended by Argus analysts and have a Thomson Reuters consensus rating of “positive,” an Argus A6 quantitative rating of “buy” and a Market Edge rating of “long”:

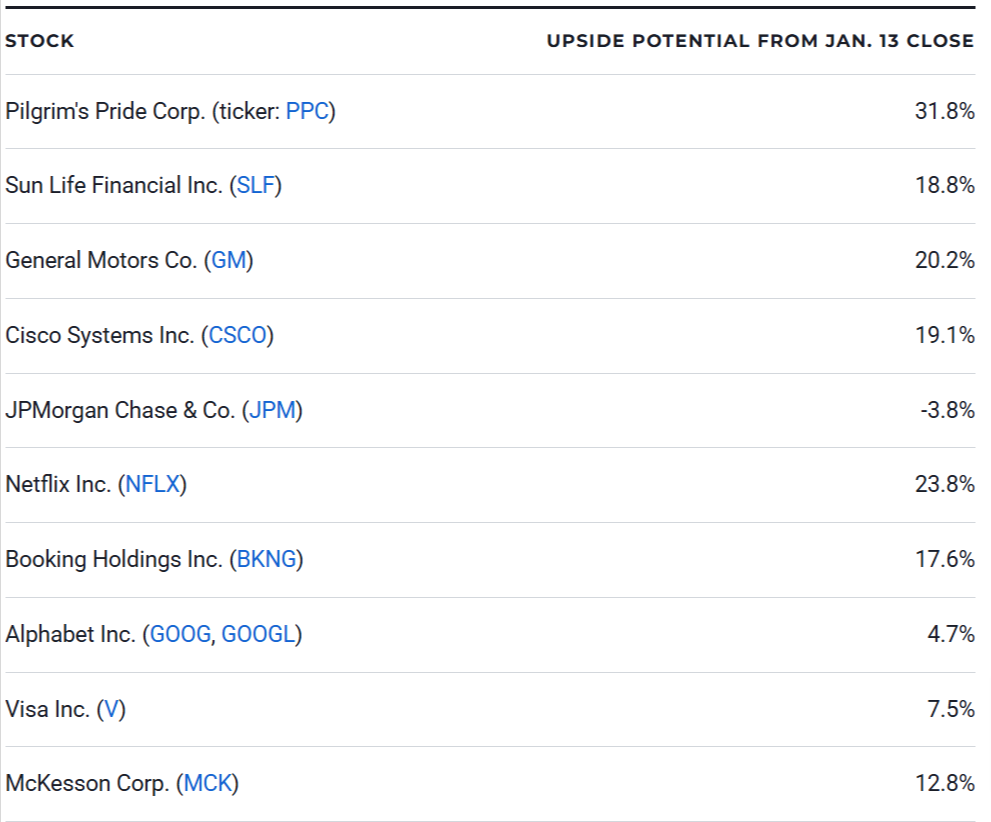

Pilgrim’s Pride Corp. (PPC)

Pilgrim’s Pride supplies fresh, frozen, and value-added chicken and pork products to distributors, retailers and foodservice operators. Argus analyst John Staszak says Pilgrim’s Pride will benefit in 2025 from higher chicken prices and restricted beef supplies. Staszak says beef shortages will stimulate more chicken purchases by both fast food chains and full-service restaurants. In addition, he says U.S. health-conscious consumers will continue to shift away from pork and beef in favor of chicken. Staszak has a bullish outlook on chicken demand in emerging markets as well. Argus has a “buy” rating and $60 price target for PPC stock, which closed at $45.53 on Jan. 13.

Sun Life Financial Inc. (SLF)

Sun Life Financial is a global financial services company that provides wealth accumulation and insurance products in Canada, the U.S., the U.K. and Asia. Analyst Kevin Heal says Sun Life is a leading Canadian insurer that is attractively valued given the company’s peer-leading returns on equity and consistent earnings strength. Its diversification, including money management and U.S., Canadian and Asian insurance sales, reduces financial risk. Heal says Sun Life has also made several opportunistic acquisitions that have boosted earnings while maintaining a healthy balance sheet. Argus has a “buy” rating and $68 price target for SLF stock, which closed at $57.23 on Jan. 13.

General Motors Co. (GM)

General Motors is the largest U.S. manufacturer of cars and trucks. GM recently announced it is shifting its autonomous vehicle technology focus from robotaxis to personal vehicles, a move that could lead to significant cost reductions and create opportunities for additional capital returns. Analyst Bill Selesky says General Motors’ strong core internal combustion engine portfolio has helped the company exceed earnings expectations. Selesky says the market is significantly undervaluing GM’s ICE business, its Ultium battery China joint venture and its financial services business. Argus has a “buy” rating and $60 price target for GM stock, which closed at $49.93 on Jan. 13.

Cisco Systems Inc. (CSCO)

Cisco Systems provides networking, cloud and cybersecurity hardware and software solutions. Argus analyst Jim Kelleher says Cisco overcame a weak spending environment among the company’s customer base in fiscal 2024, particularly among North American carriers. Kelleher says Cisco has successfully cut costs to maintain margins, and focus metric trends in remaining performance obligations, annual recurring revenue and software revenue have been solid. In the long term, Cisco’s ecosystem could play a central role in customer AI adoption. Kelleher says the company remains an attractively valued networking industry leader. Argus has a “buy” rating and $70 price target for CSCO stock, which closed at $58.76 on Jan. 13.

JPMorgan Chase & Co. (JPM)

JPMorgan Chase is one of the world’s largest banks and financial services companies with roughly $3.8 trillion in assets. In 2023, JPMorgan acquired First Republic Bank after it failed during a regional banking crisis and was seized by the Federal Deposit Insurance Corporation, or FDIC. Analyst Stephen Biggar says First Republic provided JPMorgan with a large infusion of high quality loans and deposits that will boost the bank’s high-net-worth customer base. Biggar says JPMorgan has an impressive credit card franchise and an attractive loan growth profile. Argus has a “buy” rating and $235 price target for JPM stock, which closed at $244.21 on Jan. 13.

Netflix Inc. (NFLX)

Netflix is a market leader in video streaming and has more than 280 million subscribers around the world. Analyst Joseph Bonner says Netflix implemented some bold strategies to rekindle subscriber growth in recent years, including launching an ad-supported, lower price subscription tier in 2022 and cracking down on password sharing in 2023. Looking ahead to 2025, Bonner says Netflix will focus on creating and releasing buzzworthy original content, as well as improving its content discovery process for subscribers. More live sports could enhance ad revenue as well. Argus has a “buy” rating and $1,040 price target for NFLX stock, which closed at $840.29 on Jan. 13.

Booking Holdings Inc. (BKNG)

Booking Holdings is a leading online travel platform in the U.S. and Europe and is the parent company of Priceline.com, Booking.com, Kayak.com and other leading travel and experience booking platforms. Staszak says he is bullish on online travel stocks in 2025, and Booking is a particularly compelling opportunity given its high exposure to Europe. The Booking.com brand is strong in Europe, and Staszak says Booking trades at an attractive valuation of under 22 times his 2025 earnings per share estimate. Argus has a “buy” rating and $5,600 price target for BKNG stock, which closed at $4,763.90 on Jan. 13.

Alphabet Inc. (GOOG, GOOGL)

Alphabet is one of the world’s largest online search and advertising companies and is the parent company of Google and YouTube. Bonner says Google has become somewhat of a victim of its own success in the global search business, drawing antitrust scrutiny. The company also faces artificial intelligence challenges to its online advertising dominance, but Bonner says Alphabet is taking an aggressive approach to AI by developing its own industry-leading AI features. In addition, the high-growth Google Cloud business has helped Alphabet diversify outside of advertising. Argus has a “buy” rating and $200 price target for GOOGL stock, which closed at $191.01 on Jan. 13.

Visa Inc. (V)

Visa is a global credit card leader and owner of the world’s largest electronic payment network. Biggar projects secular growth for Visa’s payment volumes in coming years and says the company can boost earnings per share further via cost cutting and share buybacks. Future catalysts include the ongoing global transition to a cashless economy, as well as growth in the company’s rewards program. Incredibly, Biggar estimates more than 80% of the world’s retail transactions are still completed with cash and checks, suggesting a massive long term opportunity for Visa. Argus has a “buy” rating and $330 price target for V stock, which closed at $306.92 on Jan. 13.

McKesson Corp. (MCK)

McKesson is one of the largest distributors of pharmaceuticals and medical-surgical supplies in the U.S. Analyst David Toung says McKesson has benefited from growing utilization of specialty and oncology drugs, as well as Ozempic and other GLP-1 obesity and diabetes drugs. Toung says McKesson has improved its profitability outlook by divesting its underperforming distribution operations in Europe and improving its Prescription Technology Solutions business. The company is focusing on its core growth strategy of expanding its distribution and technology capabilities by targeting attractive acquisitions. Argus has a “buy” rating and $660 price target for MCK stock, which closed at $585.08 on Jan. 13.