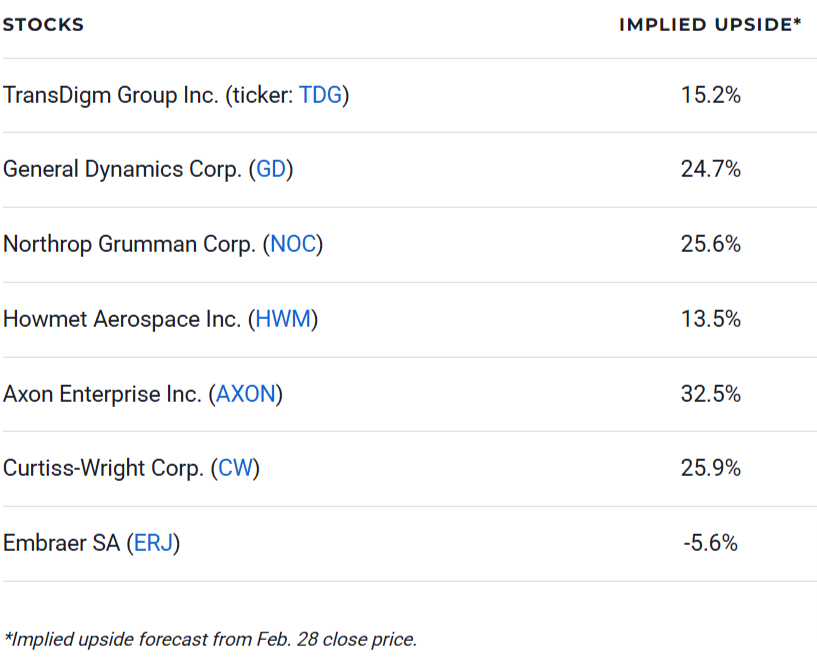

The fiscal 2025 National Defense Authorization Act (NDAA) calls for $923.3 billion in U.S. military spending, up 4.1% from 2024 levels. However, the ongoing war in Ukraine, tensions between China and Taiwan and conflicts between Israel and Iran, Hezbollah and Hamas in the Middle East may force the U.S. government to increase defense industry investment in coming years, which could serve as a tailwind for defense sector earnings. Defense stocks are attractive investments because they can often have predictable, long-term government contracts. Here are seven defense stocks to buy with big upside potential, according to Morgan Stanley:

TransDigm Group Inc. (TDG)

TransDigm designs and manufactures original aircraft parts sold to manufacturers. The company also produces aftermarket replacement parts sold to commercial and military aircraft operators. In recent years, TransDigm has announced several significant buyouts, including acquiring SEI Industries, Raptor Scientific and the components and subsystems business of Communications & Power Industries. Analyst Kristine Liwag says TransDigm’s pricing environment is positive, the commercial aircraft aftermarket is strong and the company has the financial flexibility for further capital deployment. In addition, Liwag says recent acquisitions could boost fiscal 2025 earnings. Morgan Stanley has an “overweight” rating and $1,575 price target for TDG stock, which closed at $1,367.20 on Feb. 28.

General Dynamics Corp. (GD)

General Dynamics is a diversified aerospace and defense company that produces a wide range of products, including Gulfstream jets, Abrams tanks and nuclear submarines. The majority of the company’s revenue comes from the U.S. government, particularly its large contracts with the Department of Defense. Liwag says General Dynamics’ 2025 guidance came up short of expectations, but the company’s Gulfstream G700 headwinds are finally in the rear view mirror. She says new ammunition production capacity will help boost General Dynamics’ Combat segment margins in 2025. Morgan Stanley has an “overweight” rating and $315 price target for GD stock, which closed at $252.60 on Feb. 28.

Northrop Grumman Corp. (NOC)

Northrop Grumman is one of the world’s largest weapons and military technology producers. Liwag says demand for airborne intelligence, surveillance and reconnaissance will help drive Northrop’s international revenue growth in the double digit percentage range in 2025. She says missile sales and C2 aircraft sales will also support the international business, which typically accounts for between 12% and 13% or total revenue. Liwag says Northrop is also restructuring its Defense Systems business to focus on missiles and missile defense capabilities, which are in high demand internationally. Morgan Stanley has an “overweight” rating and $580 price target for NOC stock, which closed at $461.74 on Feb. 28.

Howmet Aerospace Inc. (HWM)

Howmet Aerospace manufactures lightweight metal products, specializing in jet engine components, titanium structural parts, aerospace fastening systems and forged wheels. The company also provides defense solutions to its military partners, such as precision machining, integrated program management and metals expertise. Liwag says Howmet is a high quality aerospace supplier that will benefit from ongoing demand growth for spare engine parts. The company also produces industrial gas turbine components to meet booming power demand from artificial intelligence applications. Finally, Liwag says Howmet’s 2025 financial guidance is likely conservative. Morgan Stanley has an “overweight” rating and $155 price target for HWM stock, which closed at $136.60 on Feb. 28.

Axon Enterprise Inc. (AXON)

Axon Enterprise is a law enforcement hardware and technology solutions provider. In addition to supplying body-worn cameras and other hardware to law enforcement and military customers, Axon also provides training and cloud-based software services such as digital evidence management. Analyst Meta Marshall says Axon is generating impressive growth in both cloud and services revenue and overall annual recurring revenue. Marshall says the 25% to 30% sales growths rate Axon has generated in recent quarters could be sustainable as software accounts for a larger portion of total revenue. Morgan Stanley has an “overweight” rating and $700 price target for AXON stock, which closed at $528.45 on Feb. 28.

Curtiss-Wright Corp. (CW)

Curtiss-Wright provides specialized solutions, engineered products and other services primarily to the aerospace and defense markets. The company’s Defense Electronics segment includes products such as commercial off-the-shelf embedded computing board-level modules, integrated subsystems and data acquisition and flight test instrumentation equipment. Liwag says Curtiss-Wright’s 2025 guidance suggests the company is on track to hit the three-year financial targets management laid out at its 2024 investor day event. Those targets include greater than 5% annual organic revenue growth and above 10% annual earnings per share growth. Morgan Stanley has an “overweight” rating and $405 price target for CW stock, which closed at $321.66 on Feb. 28.

Embraer SA (ERJ)

Brazil-based Embraer is one of the world’s top regional commercial aircraft manufacturers. The company also makes private planes and military aircraft, including the Tucano single-engine pilot training and light attack aircraft. Liwag says Embraer has several key catalysts ahead that could move the stock, including additional orders of the company’s C-390 Millennium military transport aircrafts and E2 commercial jets, as well as a potential reinstatement of the stock’s dividend. She says Embraer may also eventually launch a new aircraft to compete directly with Airbus and Boeing. Morgan Stanley has an “overweight” rating and $45 price target for ERJ stock, which closed at $47.65 on Feb. 28.