January has been a rough month for Los Angeles homeowners, many of whom were victimized by the massive wildfires that engulfed vast swaths of Pacific Palisades and Malibu, among other communities.

The fire damage has been colossal, with 28 lives lost and property damage estimated in the $250 billion to $275 billion range, making it the costliest fire in U.S. history, according to Accuweather. The latest damage in Southern California exceeds the losses for the whole 2020 wildfire season.

While homeowners try to adjust to the shock, talk of rebuilding the hardest-hit L.A. communities has already commenced, with former President Joe Biden promising Uncle Sam will cover the property recovery costs for 180 days and demand already rising for contractors and equipment providers, according to a new report from Construction Dive and financial services company Baird.

That could mean a significant bump-up in several contracting industries, especially in lumber, one of the primary products needed to rebuild in the region.

With the wood-processing market growing at a 7.6% compound annual growth rate from 2024 to 2025 (to $226.2 billion), which lumber stocks will make the grade as the massive L.A. rebuild kicks off? Here’s a capsule look at seven leading stocks:

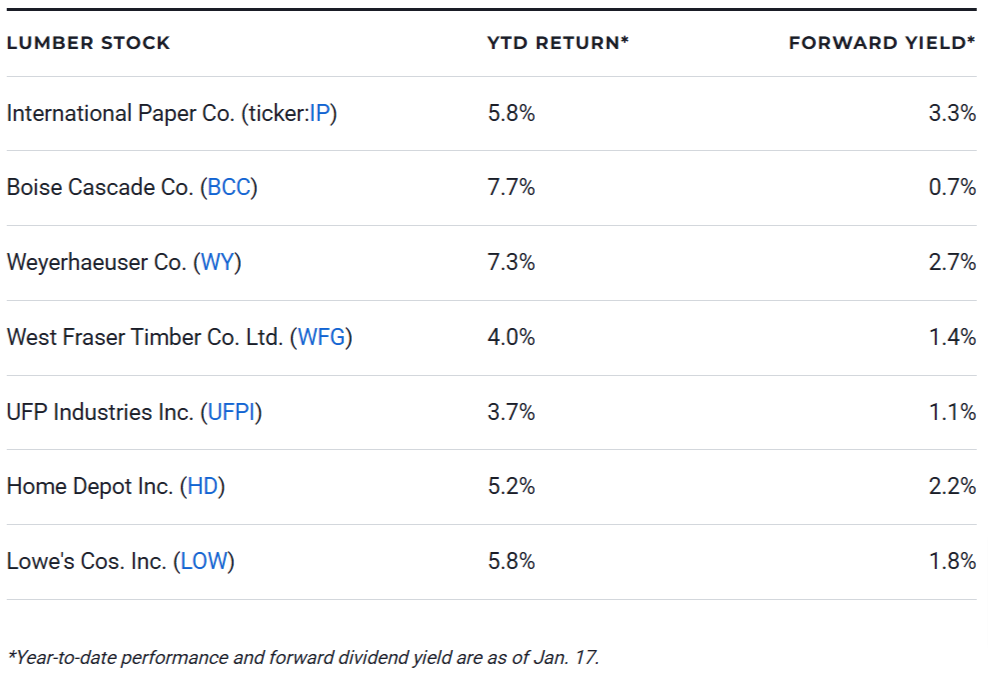

International Paper Co. (IP)

Trading around $57 per share with a three-month return of 23.1% as of Jan. 17, IP still stands as one of the tallest oaks in the lumber sector.

That’s especially the case considering its ripe 3.3% dividend yield and its planned $7.1 billion buyout of rival DS Smith, one of the eurozone’s leading paper packagers. The deal, which is expected to be formalized by Jan. 24, will make IP a worldwide leader in green-friendly packaging products and services at a time when sustainable paper solutions are trending.

Analysts jumped on the news with “buy” issues on the stock. Jefferies, for example, has reset its target price on IP shares to $66. In early January, Truist followed suit with a “buy” call on IP stock at a $65 price target. Any heightened demand for wood, pulp or paper products would likely add to the positive sentiment.

Boise Cascade Co. (BCC)

This Boise, Idaho-based engineering wood products manufacturer has taken a tumble in the past three months, losing 9.9% in share value. Yet Boise Cascade is positioned to take advantage of the rising demand for wood products from the Southern California wildfires. Its stock has jumped up 10% over the past week as of Jan. 17.

With approximately 15,000 L.A.-area buildings needing replacement, building-materials wholesaler Sherwood Lumber estimates the rebuild would require up to 20,000 truckloads of lumber. That restructuring process, which could take up to a decade or more to complete, would rely on a steady flow of lumber products to the West Coast, a job that’s ideally suited for lumber-rich Boise Cascade.

With analysts moderately souring on the stock – Loop Capital lowered its price target from $155 to $145 on Jan. 16, and Truist cut its price target from $161 to $157 – investors may also see a “buy the dip” opportunity right now with BCC.

Weyerhaeuser Co. (WY)

Seattle-based Weyerhaeuser is another lumber giant that has recently seen its share price cut down. Currently trading at $30 per share, WY shares have drifted downward by 7.3% over the past three months, although the stock has rebounded in the past week by 10.7% as of Jan. 17.

Why the roller-coaster ride? On the upside, CIBC notes that Weyerhaeuser is ideally situated if the incoming Trump administration takes a hard tariff stance against Canadian wood manufacturers.

Weyerhaeuser historically operates with some of the highest profit margins in the lumber industry and ample land to produce more lumber in a rising-demand environment, which should make the company a candidate for share-price growth in 2025. Meanwhile, earnings-per-share estimates were recently up a consensus 5.2%, according to Zacks. WY’s decent 2.7% dividend yield should also attract interest.

West Fraser Timber Co. Ltd. (WFG)

Trading at about $90 per share in the third week of January, Vancouver, British Columbia-based lumber and wood products producer West Fraser Timber has seen its shares rise by 3% over the past month as of Jan. 17. WFG’s one-year return is 11.2%.

West Fraser shares should benefit from the aging and transition of the U.S. baby boomer homeowner, although that process could take a while. Many older homeowners were able to lock in low 3% interest rates in the pandemic and are more likely to pivot to a home remodel (as many homeowners have done in the past five years) instead of selling the property.

Either way, there should be continued demand for WFG’s boards, plywood and other lumber-engineered homebuilding and remodeling projects, especially in the wildfire locales in Los Angeles, over the next several years. More moderate inflation and interest rates in early 2025 should expand that demand throughout the year, and that’s good news for West Fraser.

CIBC is supportive of better times ahead for WFG stock, with analyst Hamir Patel hiking the company’s price target from 164 Canadian dollars to CA$171 on Jan. 15. WFG also sports a 1.4% dividend.

UFP Industries Inc. (UFPI)

Founded in 1955, this Grand Rapids, Michigan-based company specializes in the supply of wood products, mainly for retail, packaging and construction. UFPI’s share price has been up 3.7% year to date, but it’s down by 13.3% over the past three months.

The company made news in early January with its purchase of C&L Wood Products, funneled through UFP Packaging LLC, a UFP affiliate. The acquisition focuses on a pair of C&L Wood specialties: pallets and mulch. The move should enhance UFP Packaging’s PalletOne enterprise, especially in northern Alabama, where C&L Wood is based. The move also leverages its $24.8 million in trailing sales, giving UFP a robust revenue stream in an industry it knows very well.

UFP is another company that should see burgeoning demand for its wood products, especially for residential home repairs. Couple that trend with the incoming demand for wood from UFPI’s mainstay retail and construction customers, and there’s a decent rationale to add UFP shares to investor portfolios before the spring homebuilding and renovation seasons begin in earnest. The stock also has a modest dividend yield of 1.1%.

Home Depot Inc. (HD)

Home Depot shares are up 17.6% over the past year and 5.2% year to date as of Jan. 17. The company makes the lumber list because it sells loads of wood and the hammers, nails, drywall and paint needed to handle major restoration jobs.

While it’s important for 10-year U.S. Treasury rates to remain around the 4.5% level or lower going forward, as high mortgage rates tend to crimp homebuilding numbers, Home Depot has a good story to tell these days. Home improvement retail sales are up 1.6% on an annual basis as of December, and growth should improve to 4.8% in April, Evercore reports.

Home Depot has also delivered on the earnings front, with third-quarter sales up 6.6% year over year and rising earnings per share. Additionally, its work upgrading its supply chain and e-commerce operations is already paying off. HD now has 19 fulfillment centers across the U.S. and can deliver goods to nine out of 10 customers within one or two days. Mix in a 2.2% dividend yield and rising demand for homebuilding and remodeling projects, and Home Depot stands out as a rising retail force in 2025.

Lowe’s Cos. Inc. (LOW)

Lowe’s stock is up 5.8% year to date thanks to a rebound over the week leading up to Jan. 17, although shares are down 6.8% over the past three months. Investors shouldn’t be too concerned; just like Home Depot, Lowe’s should stand out as home construction and remodeling rise significantly in 2025, and not just in L.A. County.

While the retailer won’t release its latest earnings numbers until the last week of February, analysts estimate a 2.3% earnings-per-share upgrade (to $1.81). Meanwhile, 20 of 34 brokerage analysts covering LOW have issued “strong buy” calls on the stock. In early January, Jefferies placed a “buy” call on LOW with a $316 price target, significantly above its current price of about $261 per share. Bernstein followed suit with a “buy” rating on the stock and a $293 price target.

LOW also comes with a solid 1.8% dividend yield, giving investors another reason to stash the stock in their portfolios in a rising year for the lumber sector.