Warren Buffett Just Bought $562 Million Worth of These 3 Stocks

Warren Buffett hasn’t seen a lot to like in the stock market lately. Through the first three quarters of 2024, Berkshire Hathaway (BRK.A 0.80%) (BRK.B 0.95%) sold $133 billion worth of stock from the portfolio he manages for the conglomerate. While he’s made a few new purchases in that time, they total just $5.8 billion.

As many stocks have seen their price rise faster than their underlying earnings, valuations are becoming stretched. It’s becoming harder and harder to find good value on Wall Street. But if you practice patience and stick to your investment objectives, you can still find plenty of opportunities.

Buffett recently found three such opportunities, and he poured over $500 million into these three companies in 2024.

Occidental Petroleum

Buffett acquired 8.9 million more shares of Occidental Petroleum (OXY 0.58%) between Dec. 17 and Dec. 19, according to filings with the SEC. He paid about $409 million total for the shares. After the purchase, Berkshire now owns approximately 28.2% of Occidental, but Buffett has said he has no plans of taking a majority stake in the business.

Still, Occidental is one of Berkshire’s largest holdings at this point. Not only does it own 28.2% of the company’s common stock, but it also owns $8.3 billion worth of preferred shares of the company, earning an 8% dividend. Those shares include warrants to buy up to 83.9 million shares of common stock for $59.62 each.

For a long time, Buffett would buy shares of Occidental whenever it traded below the price of his warrants. He’d let Occidental retire his preferred shares over time while he snatched up its common stock below his warrant price. But he’s noticeably stayed away from Occidental shares since June despite trading well below that price for months.

But at an average price of $46 per share, Buffett seems to think it’s now worth adding to his position in Occidental. Occidental owns an envious position in the Permian Basin, which is the cheapest source of oil and natural gas in the United States. However, a mild winter combined with pipeline disruptions led to significant price increases for transporting natural gas. Meanwhile, oil prices fell considerably from their 2022 highs.

But Occidental may be about turning things around. Third-quarter results came in better than expected based on strong production levels. Additionally, management laid out expectations at the start of 2024 that transport prices will move significantly lower, resulting in $300 million to $400 million per year in relative cost savings starting in the third quarter of 2025. It also expects its chemicals business to add an extra $300 million to $400 million in EBITDA once the overhaul of its Battleground chemical plant facilities in Texas is complete.

For a company that’s produced $14 billion in EBITDA over the past four quarters, an $800 million boost on top of regular operational improvements could lead to considerable growth over the next couple of years. At a current enterprise value-to-EBITDA ratio of just 5.6, Occidental shares look like a bargain. It’s no surprise Buffett couldn’t help but add more shares at this price.

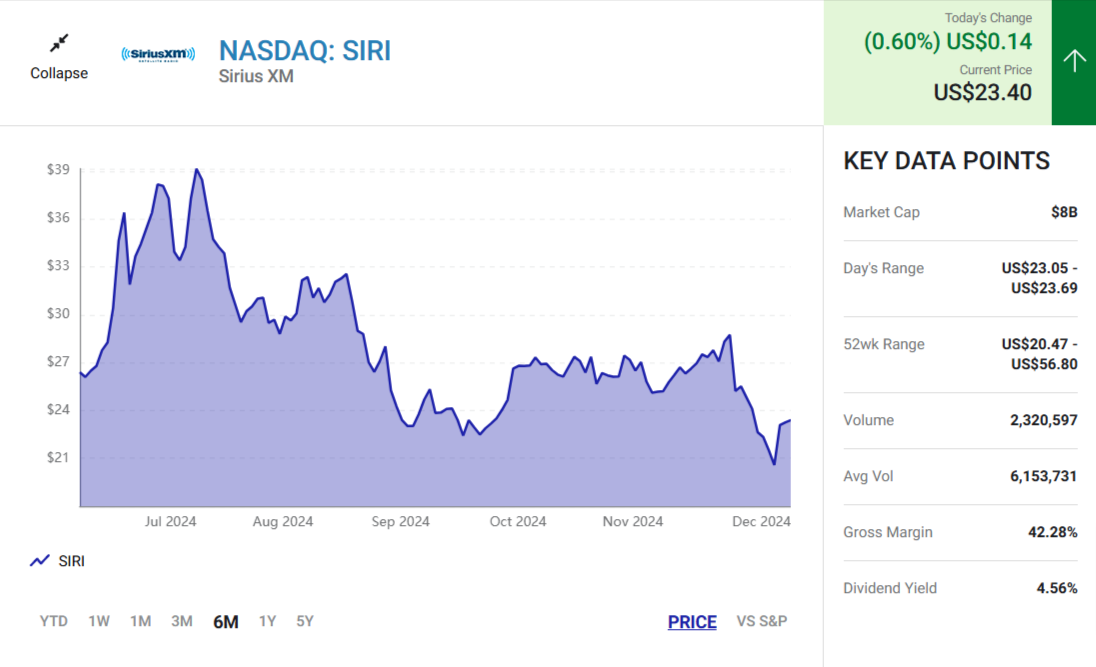

Sirius XM

Berkshire Hathaway has been accumulating shares of Sirius XM (SIRI 0.60%) since the third quarter of last year. The conglomerate previously owned nearly $1 billion worth of the company but sold off the position between 2020 and 2021. The new position is thought to be headed by Berkshire manager Ted Weschler, instead of Buffett himself.

Berkshire built its position by buying shares of Sirius XM directly, but it also bought significant amounts of the Liberty Media tracking stock, which sold at a discount to become Sirius XM shares. When the two companies merged, Berkshire found itself with about $2.5 billion worth of the company. The additional $107 million it paid for nearly 5 million more shares brought its total stake in the company to $2.7 billion.

Sirius XM management shared its 2025 outlook with investors earlier in December, disappointing many shareholders. It expects the company to generate revenue of $8.5 billion and EBITDA of $2.6 billion, both a decline from this year. On the other hand, it expects strong free cash flow conversion to provide a slight improvement in free cash flow, which it will use the majority of to pay down debt.

But buying into this weakness could be a great opportunity for investors. Management expects free cash flow to grow to $1.8 billion long-term on the back of 50 million subscribers, up from about 39 million today. Many of those subscribers may come from its app-only offering that Sirius XM is using to compete with streaming service alternatives. It also sees an opportunity with its burgeoning ad business across podcasts and a fully ad-supported offering. Declining capital expenditures will also support growing free cash flow.

Shares currently trade for around 4 times analysts’ 2025 consensus earnings estimate. That’s an extremely low price for a company that’s producing relatively stable earnings and growing free cash flow conversion.

Verisign

Buffett first acquired shares of Verisign (VRSN 0.76%) all the way back in 2012. He continued to build his position through mid-2014 but hadn’t added any more until earlier this month, when he bought $45 million worth of the domain registry service provider. The most recent purchase brings his total stake in the business to $2.6 billion, about 13.6% of the company’s shares.

Verisign controls the registry rights for .com and .net domains. It recently renewed the former contract through 2030, while the .net contract runs through mid-2029. The contract gives Verisign the right to increase the price for .com and .net domains during the last four years of their contracts by 7% and 10%, respectively.

While there are a growing number of competing top-level domains — the letters coming after the dot in a domain name — .com and .net remain by far the most popular. If you’re serious about establishing a presence online, you probably want to own a .com or .net domain. That puts Verisign in a very powerful position, and it will probably take full advantage of its ability to raise prices over time.

Verisign isn’t at much risk of losing its contracts, either. As long as it maintains certain service levels and provides critical infrastructure for the domain name system, its contracts will automatically renew. It’s been able to do just that since acquiring the rights in 2000. With a growing number of people and businesses building their own websites, it should see small annual growth in registrations combined with regular increases in its registration fees.

Verisign shares currently trade for about 23 times analysts’ consensus earnings estimate for 2025. That’s a fair price to pay for the stock, which should experience slow and steady revenue growth over time. Importantly, earnings should grow faster than revenue as price increases and the addition of new domains results in operating leverage. In a market where Buffett’s finding it harder and harder to find good value, it makes sense that he came back to this old favorite.